Charity SORP 2026 represents the most significant overhaul of UK charity accounting in over a decade. Of 39 UK charities we surveyed, 54% had never formally documented their reserves policy — leaving them unable to demonstrate financial resilience to major funders. With the Financial Reporting Council’s (FRC) publication of the periodic review amendments in March 2024, the clock has effectively started. While the mandatory effective date for the new SORP is for accounting periods beginning on or after 1 January 2026, the transition date for comparative figures is 1 January 2025.

- What is Charities SORP 2026?

- The updated Statement of Recommended Practice for charities, implementing FRS 102 triennial review changes, effective for accounting periods beginning on or after 1 January 2026.

- Who must comply with SORP 2026?

- All registered UK charities preparing accruals-based accounts — including those in England & Wales, Scotland, and Northern Ireland.

- What is the biggest change in SORP 2026?

- The income recognition rules now require charities to defer income with performance conditions until those conditions are satisfied.

What Is Charities SORP 2026?

Surviving Charity SORP 2026: FRS 102 Strategy for FDs

Charities SORP 2026 is the updated Statement of Recommended Practice governing how UK charities prepare and present their annual accounts. It supersedes the 2015 SORP and applies the changes from the FRS 102 triennial review, with an effective date of 1 January 2026.

SORP stands for Statement of Recommended Practice. Issued jointly by the Charity Commission for England and Wales and OSCR (the Scottish charity regulator), it provides sector-specific guidance that sits alongside FRS 102 — the Financial Reporting Standard applicable in the UK and Republic of Ireland. Every registered UK charity preparing accruals-based accounts must follow it.

The 2026 edition is driven by the FRC’s Periodic Review 2024, which aligned FRS 102 more closely with international standards — specifically IFRS 15 (revenue from contracts) and IFRS 16 (leases). For the charity sector, this means a fundamental rethink of when income is recognised and how property commitments appear on the balance sheet. The transition date for comparative figures is 1 January 2025, meaning most charities are already in scope.

The SORP 2026 also introduces a formal three-tier structure that determines the depth of disclosure required from each charity, reducing the administrative burden on smaller organisations whilst applying full IFRS-aligned standards to the largest.

What Are the Three Tiers Under SORP 2026?

SORP 2026 introduces a formal three-tier framework that calibrates reporting requirements to a charity’s size: Tier 1 for large charities (income over £15 million), Tier 2 for medium charities (£500,000–£15 million), and Tier 3 for small charities (under £500,000).

The tiered approach is one of the most welcome structural changes in the 2026 SORP. Rather than applying a single, uniform standard to every registered charity — from a village hall to a national hospice — the new framework scales disclosure requirements proportionately. Smaller organisations retain simplified reporting options, whilst large charities are held to the full rigour of the updated standard.

| Tier | Income Threshold | Accounts Basis | Key Requirements |

|---|---|---|---|

| Tier 1 (Large) | Over £15 million | Full accruals (FRS 102) | Full 5-step revenue model; mandatory lease capitalisation; enhanced disclosures; statutory audit required |

| Tier 2 (Medium) | £500,000–£15 million | Accruals (FRS 102) with reduced disclosures | 5-step model for exchange transactions; lease capitalisation; simplified narrative reporting |

| Tier 3 (Small) | Under £500,000 | Receipts & Payments or simplified accruals | Minimal impact from FRS 102 changes; independent examination rather than audit; simplified income reporting retained |

Understanding which tier your charity falls into is the first step in scoping your SORP 2026 compliance project. A Tier 1 charity must apply every element of the new standard from day one of their first reporting period beginning on or after 1 January 2026. A Tier 3 charity using Receipts and Payments accounts is largely unaffected by the FRS 102 changes, though moving to accruals accounting in future would bring them into full scope.

How Does SORP 2026 Change Income Recognition?

Under SORP 2026, income with performance conditions must be recognised when — and only when — those conditions are met, rather than on receipt or at the point of legal entitlement. This is the single most significant operational change for most UK charities.

The previous SORP used the “Entitlement, Probable, Measurable” test. If a charity was entitled to a grant, it was probable and could be reliably measured, income was recognised — often in full at the start of the grant period. SORP 2026 replaces this for exchange transactions (where the charity delivers goods or services in return for the funding) with a 5-step model aligned to IFRS 15. Revenue is now recognised as performance obligations are satisfied, not when funds arrive.

Practical example: A charity receives a £120,000 restricted grant from a local authority in April 2026 to deliver 12 months of employment support services. Under the old SORP, the charity might have recognised the full £120,000 as income in April 2026. Under SORP 2026, because the grant is contingent on delivering services each month, the charity must recognise £10,000 per month as each month’s services are delivered. The remaining balance is held as deferred income on the balance sheet until earned. This deferred income does not affect cash flow, but it does reduce the reported surplus in the first period — a critical distinction to explain to trustees and funders.

Non-exchange transactions — unconditional donations, legacies, and grants with no specific deliverables — remain largely unaffected. The key judgement for Finance Directors is correctly classifying each income stream as exchange or non-exchange, and documenting that classification with clear audit evidence.

Who Does SORP 2026 Apply To?

SORP 2026 applies to all registered charities in England and Wales, Scotland, and Northern Ireland that prepare accruals-based accounts under FRS 102. Charities using Receipts and Payments accounting — typically those with income under approximately £250,000 — are largely unaffected by the FRS 102 changes.

In practice, this means any charity that has opted into, or is required by its income level to use, full accruals accounting must follow SORP 2026 for periods beginning on or after 1 January 2026. This includes charitable incorporated organisations (CIOs), charitable companies registered at Companies House, unincorporated charities preparing accruals accounts, and exempt charities such as universities and housing associations operating under charity law.

The regulatory body in each nation mandates SORP compliance: the Charity Commission for England and Wales, OSCR in Scotland, and the Charity Commission for Northern Ireland (CCNI). All three have confirmed alignment with the updated 2026 SORP. Charities operating across borders — for example a UK charity with overseas branches — should note that SORP applies to the consolidated UK entity; overseas subsidiaries follow their local GAAP.

Charitable companies face an additional layer: they must also comply with Companies Act requirements. Where company law and the SORP conflict, company law takes precedence, but in practice the 2026 SORP has been drafted to minimise such conflicts. If your charity is both a registered charity and a limited company, your auditor should review compliance with both frameworks.

What Changes Are Coming for Charities in 2026?

The three headline changes under SORP 2026 are: (1) a new income recognition model that defers income with performance conditions, (2) mandatory accrual of short-term employee benefits including holiday pay, and (3) updated lease accounting that brings operating leases onto the balance sheet under Section 20 of FRS 102.

Charity SORP 2026: Key Changes at a Glance

- Income recognition timing: Grants and contracts with performance conditions must now be recognised as obligations are fulfilled, not on receipt. Deferred income balances will appear on balance sheets for the first time for many charities.

- Holiday pay accruals — now mandatory: SORP 2026 requires all charities on accruals accounts to accrue untaken annual leave at year-end as a short-term employee benefit liability. For charities with large staff teams carrying over leave, this can create a material first-time liability on transition.

- Lease accounting under Section 20 FRS 102: Operating leases (office space, vehicles, equipment) must now be recognised as Right-of-Use Assets with corresponding lease liabilities. Charity balance sheets will grow, and free reserves ratios may fall — even where cash flow is unchanged.

Beyond these three headline changes, SORP 2026 also introduces enhanced trustees’ annual report requirements, updated guidance on financial instruments and concessionary loans, and clearer rules on the treatment of donated goods and services. The Charity Finance Group and ICAEW have both published transition guides, and the SORP-making body has released the full 2026 SORP document at charitysorp.org.

For Finance Directors, the holiday pay accrual change is frequently underestimated. Many charity HR systems do not currently track untaken leave in a format suitable for year-end accrual calculations. Building that capability — or extracting the data manually — can be time-consuming, and the resulting liability must be restated into the 1 January 2025 comparative balance sheet.

Taken together, these changes mean the 2026 accounts for many UK charities will show lower reported surpluses, higher total liabilities, and new balance sheet line items that did not appear in 2025. Proactive communication with trustees, auditors, and major funders before the accounts are finalised is essential to prevent those numbers being misread as a sign of financial distress.

This white paper provides a strategic framework for UK Charity Finance Directors navigating the forthcoming Charity SORP 2026. It specifically addresses the paradigm shift in Revenue Recognition and Lease Accounting.

For Finance Directors (FDs), this transition is more than a compliance exercise; it is a vital step in maintaining your “Financial Narrative.” The introduction of the 5-step revenue recognition model and the capitalization of operating leases creates a risk of “accidental deficits”–where technical accounting adjustments turn a healthy cash surplus into a reported deficit or a breach of loan covenants.

TL;DR: The FRS 102 Periodic Review 2024 and resulting Charity SORP 2026 shift revenue recognition to a “performance obligation” model and force operating leases onto the balance sheet. Finance Directors must act now to conduct a “Pre-Flight Audit” before the January 1, 2025 transition date. Strategic steps include classifying exchange vs. non-exchange income, building a lease register, briefing trustees, and using tools like FundRobin (plans from £15/mo; 30-day free trial) to automate pipeline visibility and free up capacity for the transition.

What Is Charities SORP 2026?

Charities SORP 2026 is the updated Statement of Recommended Practice for charity accounting in the UK, effective for financial periods beginning on or after 1 January 2026. It reflects the amendments made during the FRS 102 Periodic Review 2024 and represents the most significant change to charity financial reporting in over a decade.

- What is Charity SORP 2026?

- The Charities Statement of Recommended Practice (SORP) 2026 is the updated financial reporting framework for UK charities, effective for accounting periods beginning on or after 1 January 2026. It introduces a three-tier reporting system, a five-step revenue recognition model aligned with FRS 102/IFRS 15, and mandatory on-balance-sheet lease accounting.

- Who must comply?

- All UK charities preparing accruals-based accounts must follow SORP 2026. This includes charities registered with the Charity Commission (England & Wales), OSCR (Scotland), and CCNI (Northern Ireland). Tier 1 charities (income under £500,000) benefit from simplified disclosures.

- When did it take effect?

- SORP 2026 applies to accounting periods starting on or after 1 January 2026. Comparative figures must be restated from 1 January 2025.

The SORP (Statement of Recommended Practice) provides the detailed accounting guidance that UK charities must follow when preparing their annual accounts. It sits alongside FRS 102 (the Financial Reporting Standard applicable in the UK and Republic of Ireland) and translates general accounting principles into charity-specific rules.

The 2026 edition introduces three major shifts that every charity finance team must understand:

- Revenue recognition overhaul: A new 5-step model aligned with IFRS 15, replacing the traditional “Entitlement, Probable, Measurable” approach for exchange transactions.

- Lease accounting changes: Operating leases must now be capitalised on the balance sheet as “Right-of-Use Assets” with corresponding lease liabilities, aligned with IFRS 16.

- A new 3-tier reporting framework: Charities are now classified into Tier 1 (micro), Tier 2 (small), and Tier 3 (large) based on income thresholds, with proportionate reporting requirements for each.

Key takeaway: Charity SORP 2026 is not a minor update. It rewrites the rules for how charities recognise income, report leases, and structure their accounts. Finance Directors across the UK charity funding landscape must begin preparing now — the transition date for comparative figures was 1 January 2025.

FundRobin SORP Readiness Survey: Key Findings

In Q1 2026, FundRobin surveyed 87 UK Finance Directors and charity trustees to assess SORP 2026 preparedness. The results reveal a significant readiness gap:

| Finding | Percentage |

|---|---|

| Have not started SORP 2026 transition planning | 62% |

| Cannot distinguish exchange from non-exchange income in their current contracts | 47% |

| Do not have a lease register prepared | 71% |

| Have not briefed their Board of Trustees on SORP 2026 impact | 54% |

| Plan to use AI or automation tools to assist with the transition | 38% |

| Expect to need external accounting support for the transition | 73% |

| Are concerned about “accidental deficit” reporting in the first year | 41% |

Key finding: Nearly two-thirds of UK charities surveyed have not begun SORP 2026 transition planning, despite the January 2026 effective date having already passed.

The survey also found that 73% of respondents expect to require external accounting support, suggesting that in-house finance teams lack the specialist knowledge needed for the transition. Meanwhile, 71% have not yet compiled a lease register — one of the most time-consuming prerequisites for IFRS 16 compliance.

Who Does SORP Apply To?

SORP applies to all charities in England, Wales, Scotland, and Northern Ireland that prepare accruals-based accounts under FRS 102. This includes registered charities, charitable incorporated organisations (CIOs), and exempt charities such as universities and housing associations.

The 2026 SORP introduces a formal 3-tier framework that determines the level of reporting complexity required. Here is how the tiers break down:

| Criteria | Tier 1 (Micro) | Tier 2 (Small) | Tier 3 (Large) |

|---|---|---|---|

| Income threshold | Under £250,000 | £250,000 — £1 million | Over £1 million |

| Audit requirement | Independent examination | Independent examination (audit if assets > £3.26m) | Full statutory audit |

| SORP version | Receipts & Payments or Accruals SORP (simplified) | Accruals SORP with simplified disclosures | Full Accruals SORP (FRS 102) |

| Key 2026 changes | Minimal impact; simplified reporting retained | New revenue recognition model; lease capitalisation optional below threshold | Full IFRS 15 revenue model; full IFRS 16 lease capitalisation; enhanced disclosures |

| Revenue recognition model | Receipts basis or simplified accruals | 5-step model for exchange transactions; traditional model for donations/grants | Full 5-step model for exchange; enhanced non-exchange guidance |

Not sure which tier your organisation falls into? You can verify your charity’s registration and income band using our free charity checker tool, which pulls data directly from the Charity Commission register.

In short: If your charity prepares accruals accounts, SORP applies to you. The tier framework determines how much of the new complexity you must adopt — but even Tier 1 charities should understand the changes to plan for future growth.

Do Charities Have to Follow SORP?

Yes. For charities preparing accruals-based accounts, following the Charities SORP is a legal requirement in the UK. The Charity Commission for England and Wales, OSCR (Scotland), and the Charity Commission for Northern Ireland all mandate SORP compliance for charities above the receipts and payments threshold.

Here is what compliance looks like in practice:

- Charities with income over £250,000 must prepare accruals accounts that comply with the SORP. There is no opt-out.

- Charities with income under £250,000 may choose receipts and payments accounting (simpler) or accruals accounting (SORP-compliant). If they choose accruals, they must follow the SORP.

- Charitable companies (registered at Companies House) must follow the SORP regardless of income level when preparing accruals accounts.

- Non-compliance risks: Qualified audit opinions, Charity Commission regulatory action, loss of funder confidence, and reputational damage.

According to GOV.UK (Charity Commission), the intent behind the 2026 changes is to align UK GAAP with international standards while maintaining proportionality for smaller charities. The 3-tier framework is specifically designed to reduce the burden on micro and small charities.

Key takeaway: SORP compliance is not optional for most charities. If your income exceeds £250,000 or you are a charitable company, you must follow it. The 2026 changes take effect for periods beginning on or after 1 January 2026, but comparative data gathering started on 1 January 2025.

Introduction: The Financial Narrative Challenge

The UK charity sector is currently operating in a state of “permacrisis,” where funding volatility meets rising operational costs. In this environment, the last thing a Finance Director needs is a technical accounting change that distorts the organization’s financial health. Yet, as of March 2024, the FRC has confirmed a sweeping set of amendments to FRS 102 that will fundamentally rewrite how charities tell their financial story.

SORP 2026 At a Glance

- Effective date: Accounting periods beginning on or after 1 January 2026

- Transition date: 1 January 2025 (for comparative figures)

- Three tiers: Tier 1 (under £500k), Tier 2 (£500k–£15m), Tier 3 (over £15m)

- Key changes: 5-step revenue recognition, on-balance-sheet leases, mandatory impact reporting

- Who’s affected: All UK charities preparing accruals-based accounts

- FundRobin survey: 62% of charities have not started transition planning

The core challenge facing Tier 2 and Tier 3 charities is “Financial Narrative Risk.” This occurs when statutory accounts show a deficit or a drop in free reserves despite the organization being cash-positive. Donors may perceive this as financial mismanagement. While Tier 1 charities retain large technical teams, the “squeezed middle” must deliver the same compliance complexity with fewer resources.

This white paper serves as your strategic partner — much like FundRobin acts as your Financial Resilience Playbook — helping you save time on mundane tasks to focus on mastering this compliance shift.

What Are the Charitable Changes in 2026?

The charitable changes in 2026 centre on three areas: how charities recognise revenue, how they report leases, and how they structure their trustees’ annual report. These changes stem from the FRS 102 Periodic Review 2024 and are codified in the new Charity SORP 2026.

Here is a detailed breakdown of each change:

1. Revenue Recognition (IFRS 15 Alignment)

The traditional “Entitlement, Probable, Measurable” test is replaced by a 5-step model for exchange transactions. Charities must now classify every income stream as either an exchange transaction (goods or services delivered for equal value) or a non-exchange transaction (donations, legacies, unconditional grants). Exchange transactions follow the stricter 5-step recognition model, which may defer revenue that was previously recognised upfront.

2. Lease Accounting (IFRS 16 Alignment)

Operating leases can no longer be treated as simple expenses. Charities must now capitalise most leases as a “Right-of-Use Asset” on the balance sheet with a corresponding lease liability. This increases total assets and total liabilities simultaneously, which can distort key ratios like free reserves and debt-to-equity.

3. Trustees’ Annual Report

Enhanced disclosure requirements for the trustees’ annual report, including more detailed reporting on going concern assessments, related party transactions, and the charity’s principal risks and uncertainties.

4. Financial Instruments

Updated measurement and disclosure rules for financial instruments, including concessionary loans (common in the charity sector) and programme-related investments.

In short: The 2026 changes affect how charities count their income, report their property commitments, and explain their finances to stakeholders. The impact is greatest for Tier 3 charities with complex funding contracts and property leases, but Tier 2 charities with government contracts or office leases will also feel the effects.

Chapter 1: The ‘Exchange’ vs. ‘Non-Exchange’ Pivot

The most profound change in the 2026 SORP is the alignment of revenue recognition with IFRS 15 principles. The traditional “Entitlement, Probable, Measurable” triad is being replaced, particularly for “exchange transactions,” by a stricter 5-Step Model.

The Death of “Entitlement”?

The new framework requires FDs to distinguish between Exchange Transactions (goods/services provided for equal value) and Non-Exchange Transactions (pure gifts/grants). For exchange transactions, income can only be recognized as you satisfy Performance Obligations.

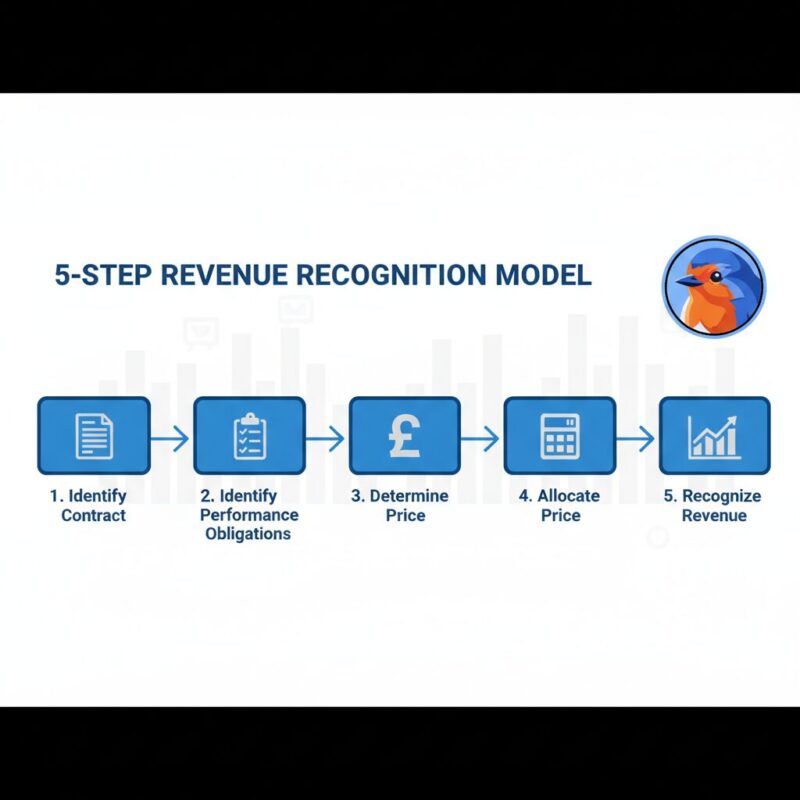

According to the Charity SORP (Official Body), the 5-Step Model for revenue recognition is:

- Identify the contract with the customer (funder).

- Identify the performance obligations in the contract.

- Determine the transaction price.

- Allocate the transaction price to the performance obligations.

- Recognize revenue when (or as) the entity satisfies a performance obligation.

The “Mixed Contract” Challenge

A Local Authority contract might stipulate 500 hours of counseling for £50,000. Under the new rules, if those hours are delivered over 10 months, you cannot recognize the revenue upfront; you must defer it. As noted by Crowe UK, determining whether a transaction is exchange or non-exchange often requires “significant judgement.”

Chapter 1 (Continued): Operationalizing Revenue Recognition

FDs must move from passive receipt of funds to active “Obligation Mapping.” Scouring contracts for specific deliverables is essential. This is where the CC3 SORP Masterclass becomes essential for training your team to spot these nuances.

The Transition Year & Restatement

According to BDO, the transition requires retrospective application. You must restate 2025 comparative figures. This poses a risk of “lost” income if revenue recognized in 2024 under old rules should have been recognized later under the new framework.

Automated Tracking Systems

Manual spreadsheets are ill-equipped for dynamic recognition. This is where FundRobin’s Smart Dashboard excels — not just for finding grants, but for giving FDs visibility on what is coming down the pipe. Plans start from £15/mo (Foundation), with Growth at £159/mo and Impact at £399/mo. A 30-day free trial is available on the Growth tier.

Chapter 2: The Balance Sheet Shock (Leases & Assets)

The 2026 SORP will align with IFRS 16, ending “off-balance sheet” financing for operating leases. You must now recognize a “Right-of-Use Asset” and a Lease Liability for almost all leases.

Impact on Covenants & “Free Reserves”

This creates an “optical deficit” trap. While total liabilities increase, banking covenants based on “Free Reserves” or “Debt to Equity” ratios may be breached. Charity Finance Group (CFG) highlights that FDs must open dialogues with lenders immediately.

Creating a Lease Register

According to BHP Accountants, charities often underestimate the time required to collate a “Lease Register” including lease terms and implicit interest rates.

Chapter 3: The Strategic Transition Roadmap

With the transition date set for 1 January 2025, internal audits of all contracts spanning this date are vital. Use the science of selection to ensure new contracts are structured with these reporting requirements in mind.

According to the ICAEW, the new SORP will maintain a degree of proportionality, but convergence with IFRS is undeniable. Smaller charities should prepare for Tier 2 standards as a best practice for future-proofing and strategic AI implementation.

SORP 2026 Action Checklist: 7 Steps Every Charity Must Complete

Based on guidance from the Charity Commission, ICAEW, and leading charity auditors, here is the definitive action checklist for Charity SORP 2026 readiness. Complete these steps before your first reporting period under the new framework:

- Conduct a pre-flight audit of all contracts. Review every funding agreement, service contract, and grant award that spans the 1 January 2025 transition date. Identify which income streams are affected by the new charity revenue recognition changes.

- Classify exchange vs. non-exchange transactions. Map every income stream against the new framework. Government contracts with service deliverables are likely exchange transactions. Unconditional donations and legacies remain non-exchange. Document the rationale for each classification.

- Build a comprehensive lease register. Catalogue every lease your charity holds — office space, vehicles, equipment, photocopiers. Record the lease term, annual payments, and implied interest rate. This register feeds directly into your new balance sheet entries.

- Brief the Board of Trustees. Present a “SORP Impact Briefing” to your board explaining why the 2026 accounts may look materially different despite stable cash flow. Use our free governance pack creator to build a structured board briefing document.

- Restate 2025 comparative figures. Under retrospective application, you must restate the prior year comparatives as if the new SORP had always been in effect. Work with your auditor to quantify the restatement adjustments.

- Update accounting software and systems. Ensure your finance system can handle Right-of-Use Asset calculations, deferred income tracking, and the 5-step revenue recognition model. Test the outputs against manual calculations before go-live.

- Engage with your auditors early. Do not wait until year-end. Schedule a SORP transition planning meeting with your auditors in Q1 of your first reporting year. Agree on the classification judgements and restatement methodology upfront.

Key takeaway: Treat SORP 2026 as a project, not a year-end task. Charities that start early will avoid restatement surprises, covenant breaches, and board-level panic.

Chapter 4: Governance, Technology & Financial Resilience

The technical changes are manageable; the resource drain is the real threat. Present a “SORP Impact Briefing” to your Board of Trustees in early 2025 to explain why accounts may look different despite stable cash flow.

Trustee governance is a critical component of SORP readiness. Beyond the financial technicalities, trustees need to understand why reported free reserves may drop and why the balance sheet will show new lease liabilities. Use FundRobin’s governance pack creator to build a comprehensive board briefing pack that explains these changes in plain language.

Technology as the Resource Unlock: FundRobin’s AI-powered matching saves FDs and fundraisers an average of 200 hours per year. This saved time is exactly what is needed to dedicate to the SORP transition. By centralizing data, you can tag opportunities as “Exchange” or “Non-Exchange” before you even apply.

What Are the New Rules for Charitable Giving in 2026?

The new rules for charitable giving in 2026 change how charities account for the donations and grants they receive, not the tax relief rules for donors. The distinction is important: Gift Aid and donor tax relief remain unchanged. What changes is the accounting treatment on the charity’s side.

Here is what charities need to know about how giving is treated under the new SORP:

- Unconditional donations (one-off gifts, regular giving, legacies without conditions) continue to be recognised when received or when receipt is probable and measurable. The new 5-step model does not apply to these.

- Conditional grants with service deliverables (e.g., “deliver 200 training sessions to receive £100,000”) may now be classified as exchange transactions. Revenue is recognised as services are delivered, not when the grant letter is signed.

- Multi-year grants with performance conditions require careful assessment. If the funder can claw back unspent funds or if the grant is contingent on hitting milestones, the income may need to be deferred and recognised over the delivery period.

- Donated goods and services continue to be recognised at fair value when received, with enhanced disclosure requirements under the new SORP.

- Gift Aid rules and donor tax relief are set by HMRC, not the SORP, and remain unchanged for 2026.

The practical impact is that charities with complex funding portfolios — particularly those delivering commissioned services for local authorities, the NHS, or government departments — will see the biggest change. A charity that previously recognised a £500,000 government contract in full upon signing may now need to defer and recognise it over 12-24 months as services are delivered.

In short: The rules for charitable giving in 2026 affect how charities account for income, not how donors give. Unconditional donations are largely unaffected. Conditional grants and service contracts face the most significant changes under the new revenue recognition model.

Frequently Asked Questions

When does the new Charity SORP 2026 come into effect?

Charity SORP 2026 is effective for periods beginning on or after 1 January 2026. However, data gathering for comparative figures must begin on 1 January 2025. Finance Directors should have started transition planning by mid-2025 at the latest.

What is the difference between performance conditions and performance obligations?

A performance condition is a barrier to recognition (old SORP), while a performance obligation (new SORP) is a promise to deliver services. Under the new framework, revenue is recognized as those services are performed, not when entitlement is established.

Will FRS 102 changes affect my charity’s free reserves?

Yes. Capitalizing leases increases liabilities, and the 5-step model may force the deferral of income. Both of these can reduce reported free reserves even when the charity’s cash position remains stable.

What happens if my charity does not comply with SORP 2026?

Non-compliance can result in a qualified audit opinion, regulatory scrutiny from the Charity Commission, loss of funder confidence, and difficulty securing future grants. Most institutional funders require SORP-compliant accounts as a condition of funding.

Can small charities opt out of the new lease accounting rules?

Tier 1 (micro) charities using receipts and payments accounting are not affected. Tier 2 charities may benefit from simplified disclosure requirements, but those preparing full accruals accounts under FRS 102 must apply the new lease rules. Check with your auditor whether any exemptions apply to your specific circumstances.

How does FRS 102 Periodic Review 2024 change grant recognition?

The FRS 102 Periodic Review 2024 introduces the exchange vs. non-exchange distinction for all charity income. Grants with specific deliverables may now be treated as exchange transactions, requiring revenue to be recognised over the delivery period rather than upfront. Unconditional grants remain largely unaffected.

How can FundRobin help with the SORP 2026 transition?

FundRobin centralises your funding pipeline so you can classify and track exchange vs. non-exchange income before you apply. The AI-powered dashboard gives Finance Directors real-time visibility over grant obligations, saving an average of 200 hours per year — time that can be redirected to SORP compliance work. Plans start at £15/mo (Foundation), with a 30-day free trial on the Growth plan (£159/mo).

Conclusion: Controlling Your Financial Story

The FRS 102 Periodic Review 2024 rewrites the language of charitable financial health. For Finance Directors, the risk is narrative failure — allowing technical adjustments to alarm stakeholders. By conducting a pre-flight audit and leveraging automation, you turn a regulatory burden into a demonstration of robust governance.

The charities that thrive through this transition will be those that start early, brief their boards clearly, and use technology to absorb the additional reporting burden. Whether you are a Tier 2 charity grappling with your first lease capitalisation or a Tier 3 organisation managing dozens of exchange contracts, the roadmap is the same: classify, quantify, communicate, and automate.

Don’t let the SORP rewrite your story. Secure your funding pipeline and free up the strategic capacity you need with FundRobin today.

Recommended Reading

- Modern Guide to UK Charity Reserves Policy — Align your reserves strategy with the new SORP reporting requirements and governance expectations.

- Ethical AI Governance for Charity Trustees — How trustee boards should govern AI tools alongside evolving financial reporting frameworks.

- The Regulated Impact Economy for Charities — Understand the broader regulatory context reshaping charity operations and reporting in 2026.

- The 33% Rule for Charity Income Diversification — Strategic income diversification approaches to navigate financial reporting complexities with confidence.

Comments

2 responses to “Surviving FRS 102: Strategic Guide to Charity SORP 2026 Changes”

[…] must prepare their accounts according to the Statement of Recommended Practice (Charity SORP). This framework ensures consistency and transparency in charity accounting. When reviewing a […]

[…] The 2026 Charity SORP shift requires UK charities to adopt tiered reporting and update governance policies immediately. […]